Understanding Loan Terms and Interest Rates for International Fix and Flip Investors

November 28, 2024

Fix and flip loans are a key tool when investing in U.S. real estate. For foreign investors, the fix and flip strategy offers an exciting opportunity to profit by buying, renovating, and reselling properties.

And yes, you can obtain loans to make this happen.

But, understanding the specific loan terms and interest rates available to international investors is key to maximizing your potential returns from fixing and flipping real estate.

This blog will provide you with the essential insights and steps needed to successfully obtain fix and flip loans in the U.S. After reading, you’ll be well-equipped to tap into the fix and flip market in the United States.

House Flipping Activity in the U.S.

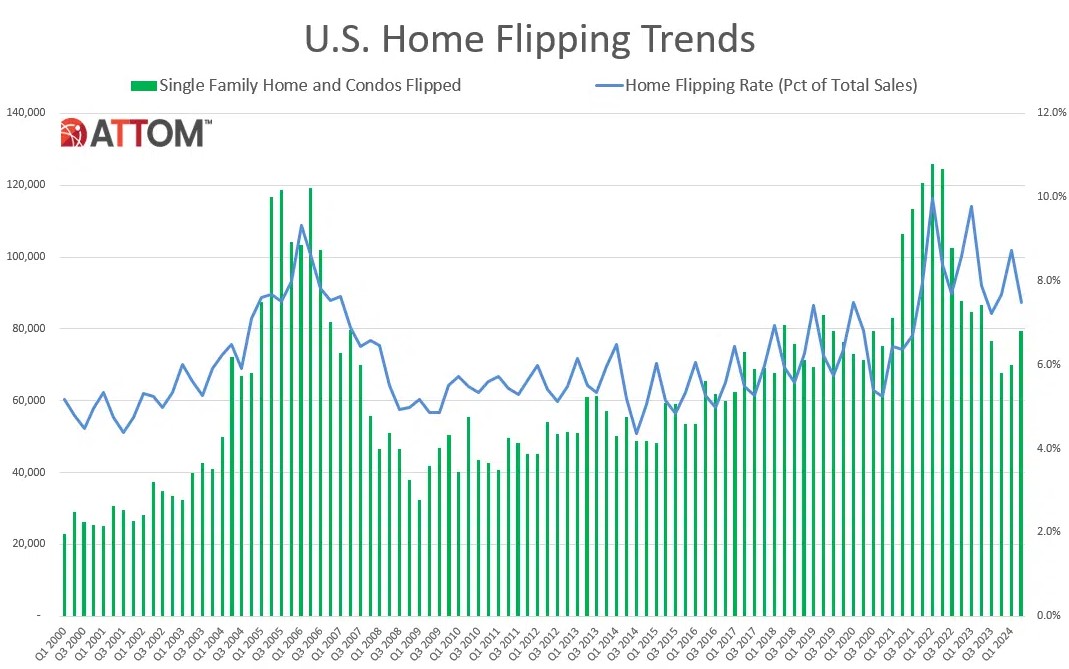

According to ATTOM’s Q2 2024 U.S. Home Flipping Report, house flipping activity has seen some interesting shifts. While the flipping rate decreased to 7.5% of all home sales in Q2 2024, down from 8.7% in Q1, profits for investors have been inching upward.

The typical profit margin on flipped homes reached 30.4% nationwide, marking the fourth increase in five quarters. This translates to a gross profit of about $73,500 per flip. However, it’s important to note that these figures are still below the peaks seen in 2016 and could be affected by various expenses like renovation costs and property taxes.

As you consider your investment strategy, keep in mind that flipping rates and profit margins vary significantly across different metro areas. For instance, cities like Warner Robins, GA, and Atlanta, GA, have seen higher flipping rates, while markets like Hilo, HI, and San Jose, CA, have experienced lower rates but potentially higher gross profits.

How To Get Started With Fix and Flip Loans

Fix and flip loans are short-term financing options designed to help investors purchase, renovate, and sell properties for a profit. These loans are typically used for residential properties, including single-family homes, condos, and smaller multi-family units. The main appeal lies in their flexibility, allowing you to secure funds fast and focus on quickly turning a property around at a profit.

As a foreign national looking for fix and flip loans, you’ll find that eligibility criteria are generally more flexible compared to traditional mortgages. If you’re a U.S. citizen, you typically need a minimum credit score of 680, though some lenders may accept scores as low as 620. If you’re a foreign national, no credit score is required. But understanding foreign investor rates is still important for business planning.

You’ll also need to demonstrate a strong financial position, including proof of income and assets. Most lenders require a down payment of at least 20% to 30% of the property’s purchase price, but this can vary depending on the specific lender and your financial profile.

As a foreign national, you will need to provide additional documentation to verify your identity and financial status. This includes copies of your passport, visa, and international credit reports or bank statements. Some lenders may also require you to have a U.S. bank account or a guarantor.

When applying for a fix and flip loan, you’ll need to present a detailed project plan and budget for the property renovation. Lenders will want to see that you have a clear strategy for improving the property’s value and a realistic timeline for completing the work.

They may also consider your experience in real estate investing and property renovation when evaluating your application. Remember that fix and flip loans are typically short-term, ranging from 1 to 18 months, so you’ll need to demonstrate your ability to complete the project and repay the loan within this timeframe.

Understanding Fix and Flip Interest Rates

Fix and flip interest rates for property in the U.S. typically begin at 9.99%, depending on various factors such as your credit score, experience, and the specific lender.

These fix and flip interest rates are generally higher than traditional mortgages due to the short-term nature and increased risk associated with fix and flip projects. In addition to interest, you should be prepared for origination fees, which can range from 1% to 3% of the loan amount, and other closing costs.

The loan-to-cost (LTC) and after-repair loan-to-value (ARLTV) ratios offered by lenders often depend on your level of experience as an investor. If you’re a beginner, you might expect LTC ratios around 80% and ARLTV ratios of 65%.

More experienced investors with a proven track record may qualify for higher ratios, potentially up to 90% LTC and 70% ARLTV. These higher ratios can significantly reduce your out-of-pocket expenses and increase your potential return on investment. But, keep in mind that higher LTC and ARLTV ratios may also come with slightly higher interest rates or fees to offset the increased risk to the lender.

Loan Terms for Fix and Flip Properties

Loan criteria, including loan pricing, for fix and flip loans can be tailored to the unique needs of foreign property investors in the U.S. Typically, these loans range from $75,000 to $5 million, allowing you to finance various property sizes and types.

The purpose of these loans is primarily for the purchase and renovation of non-owner occupied residential properties, including single-family homes, multi-family units, and sometimes even small commercial properties. This flexibility allows you to pursue a wide range of fix and flip investment opportunities in the U.S. real estate market.

The loan terms for fix and flip properties are generally short-term, ranging from 1 to 18 months. This timeframe is designed to align with the typical duration of a renovation and resale project. Most lenders offer interest-only payments during the loan term. This positively impacts the overall loan pricing, helping you manage cash flow during the renovation phase.

It’s important to note that many fix and flip loans come with no prepayment penalties, allowing you to pay off the loan early without additional costs if you complete your project ahead of schedule.

Seizing Opportunities in the U.S. Fix and Flip Market

The U.S. fix and flip market offers substantial opportunities for international investors, especially when leveraging favorable fix and flip interest rates. With the right approach to understanding fix and flip interest rates and loan terms, you can maximize your potential returns.

In this blog post, we’ve explored the key loan terms for fix and flip financing, including how different foreign investor rates can impact your bottom line. By familiarizing yourself with loan pricing, you can make more strategic decisions that align with your investment goals.

By seizing these opportunities, you position yourself to benefit from the U.S. fix and flip market’s profit potential. With the right interest rates, loan pricing, and favorable foreign investor rates, you’re well-equipped to take strategic steps toward successful property investments in the U.S.

*The information contained in this post has been provided by Lend A.I. Ltd. (and/or its affiliates) for information purposes only, and as such, this post shall not be interpreted as legal, tax, professional, or commercial advice. While every care has been taken to ensure that the content is useful and accurate, Lend A.I. (and/or its affiliates) gives no guarantees, undertaking or warranties in this regard, and does not accept any legal liability or responsibility for the content or the accuracy of the information so provided, or, for any loss or damage caused arising directly or indirectly in connection with reliance on the use of such information.